Mathematical Foundations of the DDM

Dogukan Nami Oztas

2025-05-19

Introduction

While our project primarily focuses on understanding the Diffusion Decision Model (DDM) through simulation, it’s important to recognize that the DDM is a formally defined mathematical model. The simulations we perform are essentially numerical approximations of an underlying continuous stochastic process. This vignette provides a brief conceptual overview of these mathematical foundations.

The DDM: A Continuous Process of Evidence Accumulation

At its heart, the DDM describes how evidence (\(X_t\)) for one of two choices accumulates over time (\(t\)). This accumulation isn’t perfectly steady; it’s influenced by two main forces:

- A systematic “pull” or “drift”: This is the average direction and speed at which evidence tends to accumulate, represented by the drift rate (\(v\)). A stronger or clearer stimulus generally leads to a higher magnitude of \(v\).

- Random “jiggles” or “noise”: This represents moment-to-moment fluctuations and inconsistencies in the evidence gathering or processing, characterized by a noise standard deviation (\(s\)).

To describe such a continuous process that changes both systematically and randomly, mathematicians use Stochastic Differential Equations (SDEs).

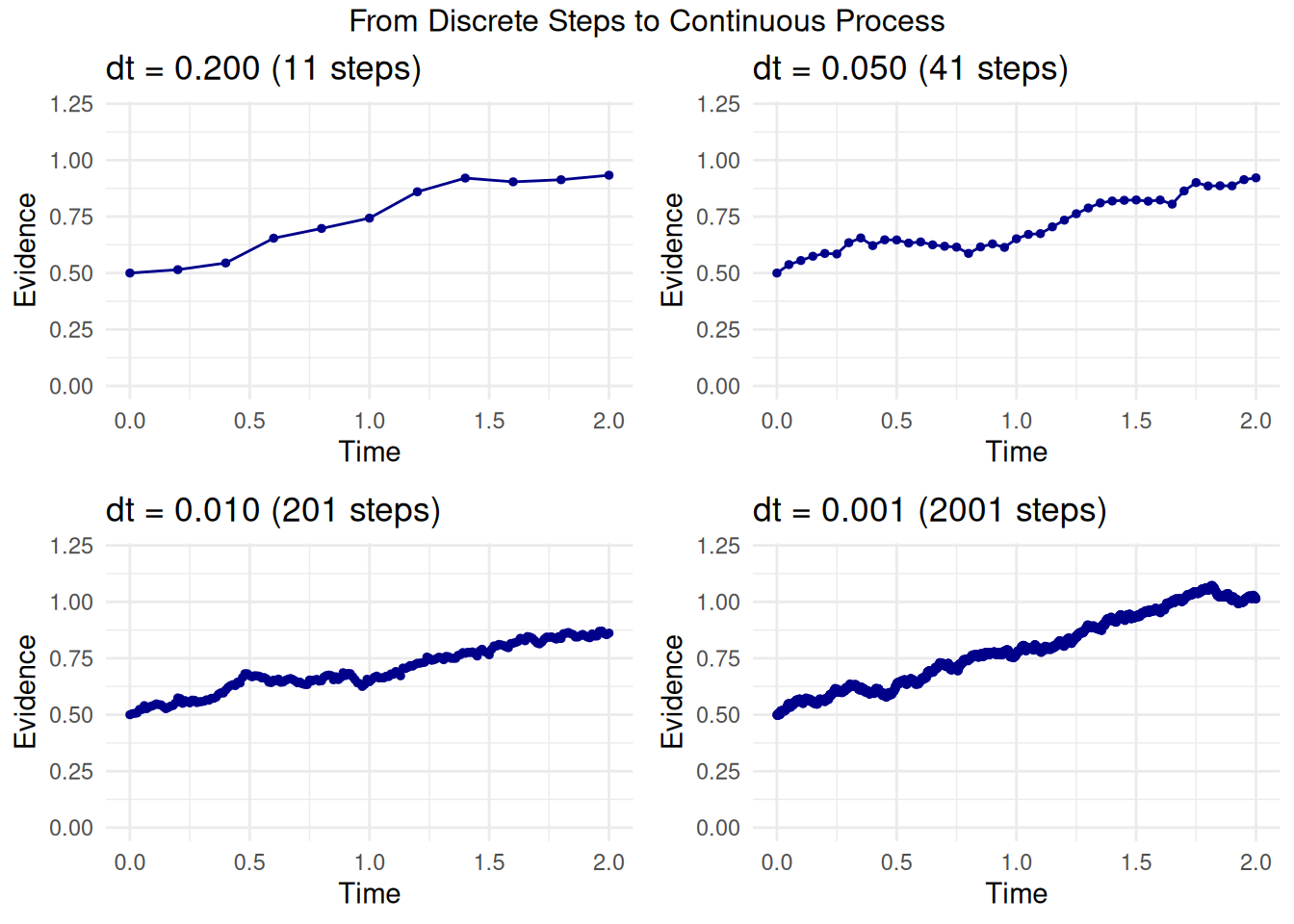

Understanding “Infinitesimal” and Continuous Change

Before looking at the SDE, let’s understand the concept of “infinitesimal.” Imagine trying to describe a smooth, curved path:

- You could use a few straight line segments connecting distant points. This would be a rough approximation.

- You could use many, many very short line segments. This would look much smoother and closer to the true curve.

“Infinitesimal” takes this idea to the extreme: it refers to changes or intervals that are immeasurably or incalculably small. By considering these infinitely small steps in time (\(dt\)) and evidence (\(dX_t\)), calculus and SDEs can precisely describe processes that unfold continuously and smoothly, even when they involve randomness.

The DDM as a Stochastic Differential Equation (SDE)

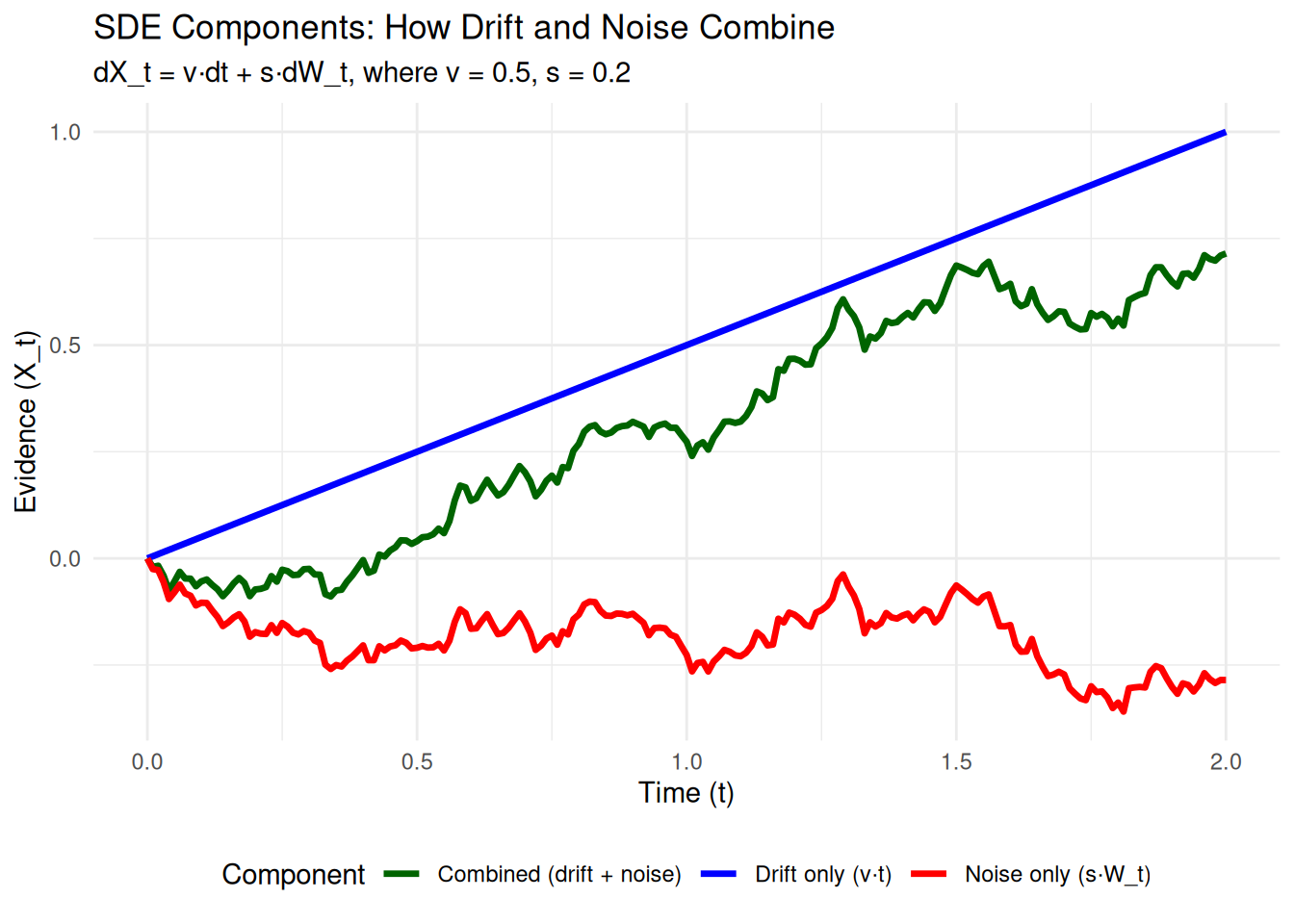

The DDM’s evidence accumulation process is formally expressed by the following SDE:

\[ dX_t = v \cdot dt + s \cdot dW_t \]

Let’s break this down:

- \(dt\) (Infinitesimal Time Step): Think of this as an incredibly tiny, almost zero-length, slice of time.

- \(dX_t\) (Infinitesimal Change in Evidence): This is the tiny change in the accumulated evidence \(X\) that happens during that infinitesimal time \(dt\).

- \(v \cdot dt\) (The Drift

Component):

- \(v\) is the drift rate.

- This term represents the predictable, average change in evidence due to the quality of the stimulus. If there were no noise, the evidence would change by exactly \(v \cdot dt\) during the time \(dt\).

- \(s \cdot dW_t\) (The

Noise/Diffusion Component):

- \(s\) is the noise intensity (standard deviation of the noise process).

- \(dW_t\) is an infinitesimal increment of a Wiener process (also known as Brownian motion). You can think of \(dW_t\) as a tiny, random “kick” or “nudge” the evidence receives during \(dt\). These kicks are drawn from a Normal distribution with a mean of 0 and a variance equal to \(dt\) (so, standard deviation \(\sqrt{dt}\)). The \(s\) parameter scales the size of these random kicks.

So, the equation \(dX_t = v \cdot dt + s \cdot dW_t\) means: “In an infinitesimally small moment of time \(dt\), the tiny change in evidence \(dX_t\) is the sum of a systematic change due to drift (\(v \cdot dt\)) and a random change due to noise (\(s \cdot dW_t\)).”

Connecting the SDE to Our Simulations (Euler-Maruyama)

Computers can’t work with true “infinitesimals.” Instead, our

simulation functions (like simulate_diffusion_trial) use a

small, finite time step, which we call dt

in our code (e.g., 0.001 seconds). This method of

approximating an SDE with small, discrete steps is known as the

Euler-Maruyama method.

For each small time step dt in our simulation, the

change in evidence (\(\Delta X_t\)) is

calculated as:

\[ \Delta X_t \approx v \cdot \text{dt}_{\text{sim}} + s \cdot \sqrt{\text{dt}_{\text{sim}}} \cdot Z \]

where: * \(\text{dt}_{\text{sim}}\) is our simulation’s time step parameter. * \(Z\) is a random number drawn from a standard Normal distribution (mean 0, standard deviation 1).

This simulated increment

rnorm(1, mean = v_trial * dt, sd = s * sqrt(dt)) directly

implements this Euler-Maruyama step. The smaller we make our simulation

dt, the closer our simulated paths get to the true

continuous process described by the SDE. It’s like using more and more

tiny line segments to draw a smooth curve.

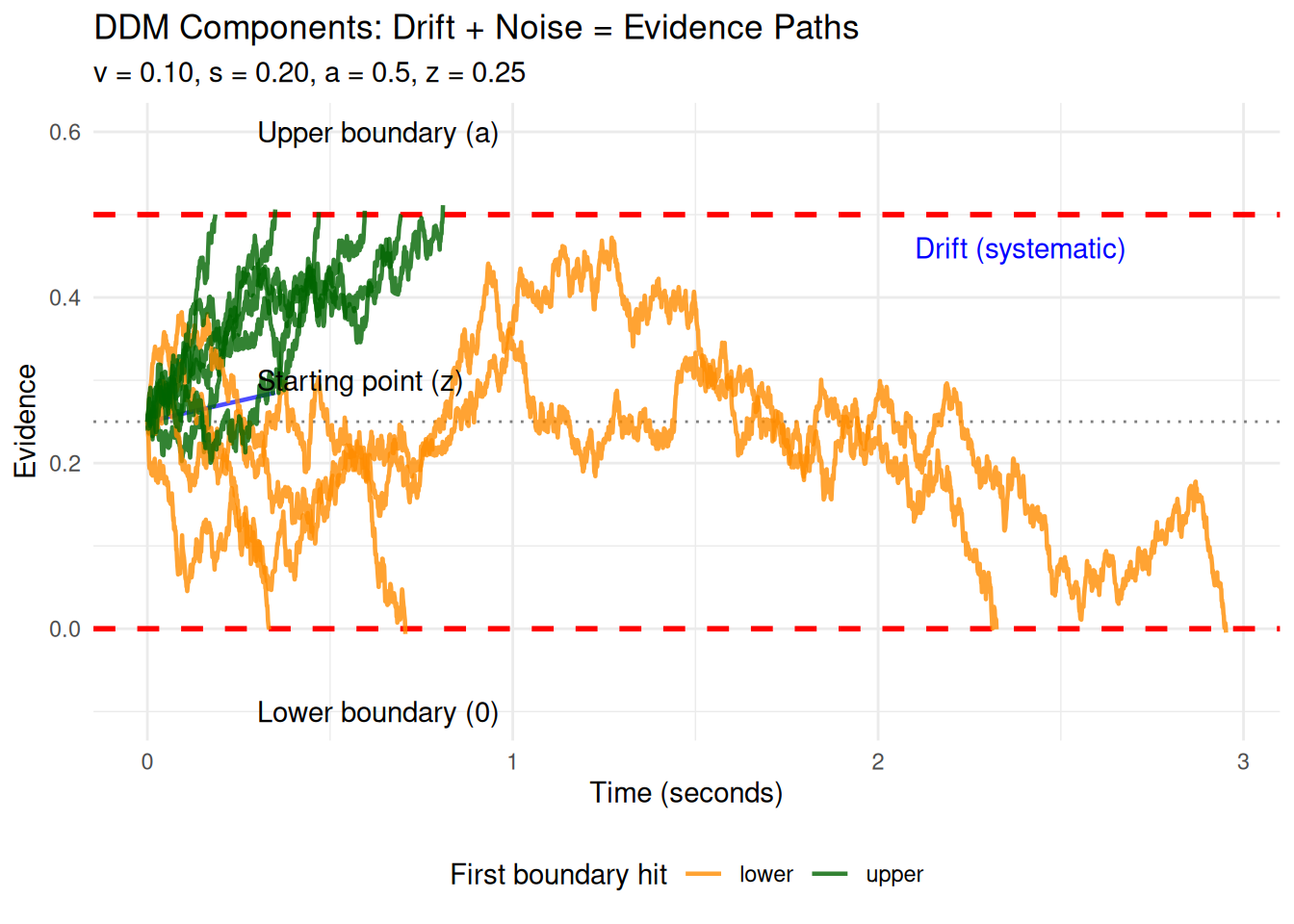

First Passage Times and Choice Probabilities

The core predictions of the DDM concern two main outcomes:

- Choice: Which of the two decision boundaries (e.g., an upper boundary \(a\) or a lower boundary \(0\)) is the accumulating evidence \(X_t\) going to hit first?

- Reaction Time (RT): How long does it take for the evidence to reach one of these boundaries? In mathematical terms, this is known as a “first passage time” – the time it takes for the process to first cross a specific threshold.

For the simple DDM, where the parameters

v (drift rate), a (threshold separation),

z (starting point), and s (noise intensity)

are all constant across trials, mathematicians like William Feller have

derived analytical solutions.

What is an Analytical Solution?

An analytical solution is a precise mathematical formula that directly calculates a model’s prediction (like a choice probability or the shape of the RT distribution) from its parameters. This is different from a simulation, which approximates these predictions by running many random trials. Analytical solutions are exact and computationally efficient when available.

These solutions often come from solving the differential equations (like the Kolmogorov equations) associated with the stochastic process defined by the DDM. Feller’s work provided many foundational results for such diffusion processes.

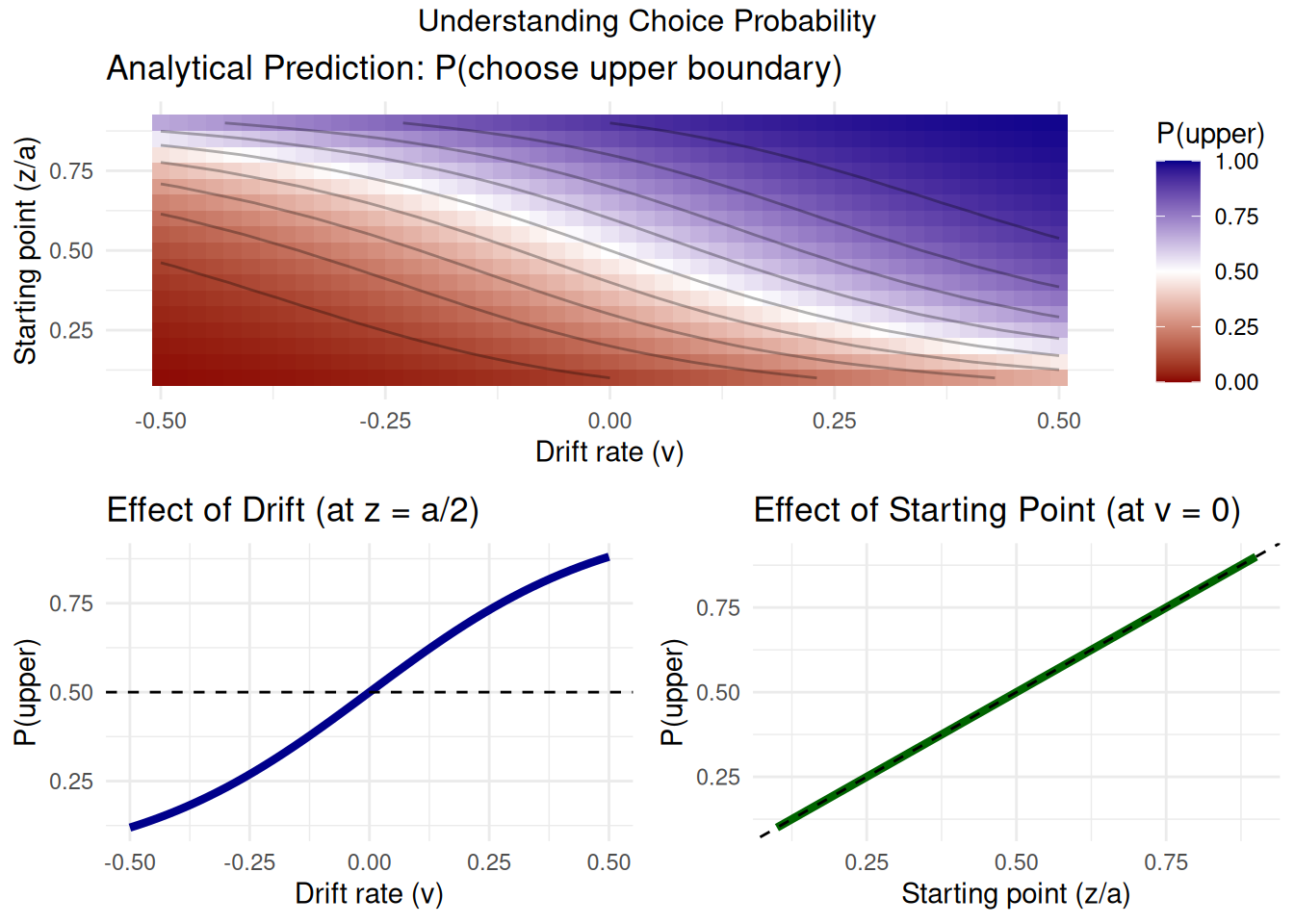

Analytical Solution for Choice Probability

One such key analytical result, derived from the theory of diffusion processes (see Feller, 1968, Vol II, Ch. XIV), gives us the probability that the evidence accumulation process, starting at \(z\) with boundaries at \(0\) and \(a\), will hit the upper boundary \(a\) before hitting \(0\).

For \(v \neq 0\), this probability is:

\[ P(\text{hit upper } a) = \frac{1 - e^{-2vz/s^2}}{1 - e^{-2va/s^2}} \]

And if \(v = 0\):

\[ P(\text{hit upper } a) = \frac{z}{a} \]

We can implement this formula in R and compare its predictions to

those from our DDM simulator (the version without across-trial

parameter variability, found in

R/02_ddm_simulator_basic.R). This comparison serves as an

important validation of our simulation code.

analytical_p_upper <- function(v, a, z, s) {

if (a <= 0 || z < 0 || z > a || s <= 0) { # Basic validation

warning("Invalid parameters for analytical_p_upper.")

return(NA)

}

if (abs(v) < 1e-9) { # Treat v as effectively zero

return(z / a)

} else {

# Using s directly as in dX = v*dt + s*dW, so s^2 is variance rate parameter

numerator <- 1 - exp(-2 * v * z / (s^2))

denominator <- 1 - exp(-2 * v * a / (s^2))

if (abs(denominator) < 1e-9) { # Avoid division by zero if exp terms are ~1

warning("Denominator close to zero in analytical_p_upper; parameters might be extreme.")

return(NA)

}

return(numerator / denominator)

}

}Comparing Analytical Solution with Simulation

Let’s pick a set of parameters and see how our simulation results for P(choice=1) compare to the analytical solution.

# Parameters for comparison

comp_params_math <- list(

v = 0.1,

a = 0.7,

z = 0.35, # Unbiased start

s = 0.2, # Standard DDM scaling parameter for s

ter = 0, # Not relevant for choice probability, set to 0 for this sim

dt = 0.001

)

n_sim_math_comp <- 2000 # Use a large number of trials for stable estimate

# Analytical Prediction

p_upper_analytical_val <- analytical_p_upper(

v = comp_params_math$v, a = comp_params_math$a,

z = comp_params_math$z, s = comp_params_math$s

)

cat(paste("Analytical P(hit upper boundary 'a'):", round(p_upper_analytical_val, 5)), "\n")## Analytical P(hit upper boundary 'a'): 0.85195# Simulation (using simulate_diffusion_experiment from 02_ddm_simulator_basic.R)

set.seed(2024)

sim_data_math_comp <- simulate_diffusion_experiment(

n_trials = n_sim_math_comp,

v = comp_params_math$v,

a = comp_params_math$a,

z = comp_params_math$z,

s = comp_params_math$s,

ter = comp_params_math$ter,

dt = comp_params_math$dt

)

p_upper_simulated_val <- mean(sim_data_math_comp$choice == 1, na.rm = TRUE)

cat(paste("Simulated P(hit upper boundary 'a') from", n_sim_math_comp, "trials:", round(p_upper_simulated_val, 5)), "\n")## Simulated P(hit upper boundary 'a') from 2000 trials: 0.85179cat(paste("Absolute difference:", round(abs(p_upper_analytical_val - p_upper_simulated_val), 5)), "\n")## Absolute difference: 0.00016# Comprehensive comparison of analytical vs simulated

verify_analytical_solution <- function(n_sims = 1000) {

# Test parameters

test_params <- expand.grid(

v = c(-0.3, -0.1, 0, 0.1, 0.3),

z_ratio = c(0.3, 0.5, 0.7)

)

test_params$a <- 1.0

test_params$z <- test_params$z_ratio * test_params$a

test_params$s <- 0.5

results <- data.frame()

for (i in 1:nrow(test_params)) {

params <- test_params[i,]

# Analytical prediction

p_analytical <- analytical_p_upper(params$v, params$a, params$z, params$s)

# Simulation

sim_data <- simulate_diffusion_experiment(

n_trials = n_sims,

v = params$v,

a = params$a,

z = params$z,

s = params$s,

ter = 0,

dt = 0.001,

verbose = FALSE

)

p_simulated <- mean(sim_data$choice == 1, na.rm = TRUE)

se_simulated <- sqrt(p_simulated * (1 - p_simulated) / n_sims)

results <- rbind(results, data.frame(

v = params$v,

z_ratio = params$z_ratio,

p_analytical = p_analytical,

p_simulated = p_simulated,

se_simulated = se_simulated,

difference = p_simulated - p_analytical

))

}

# Visualization

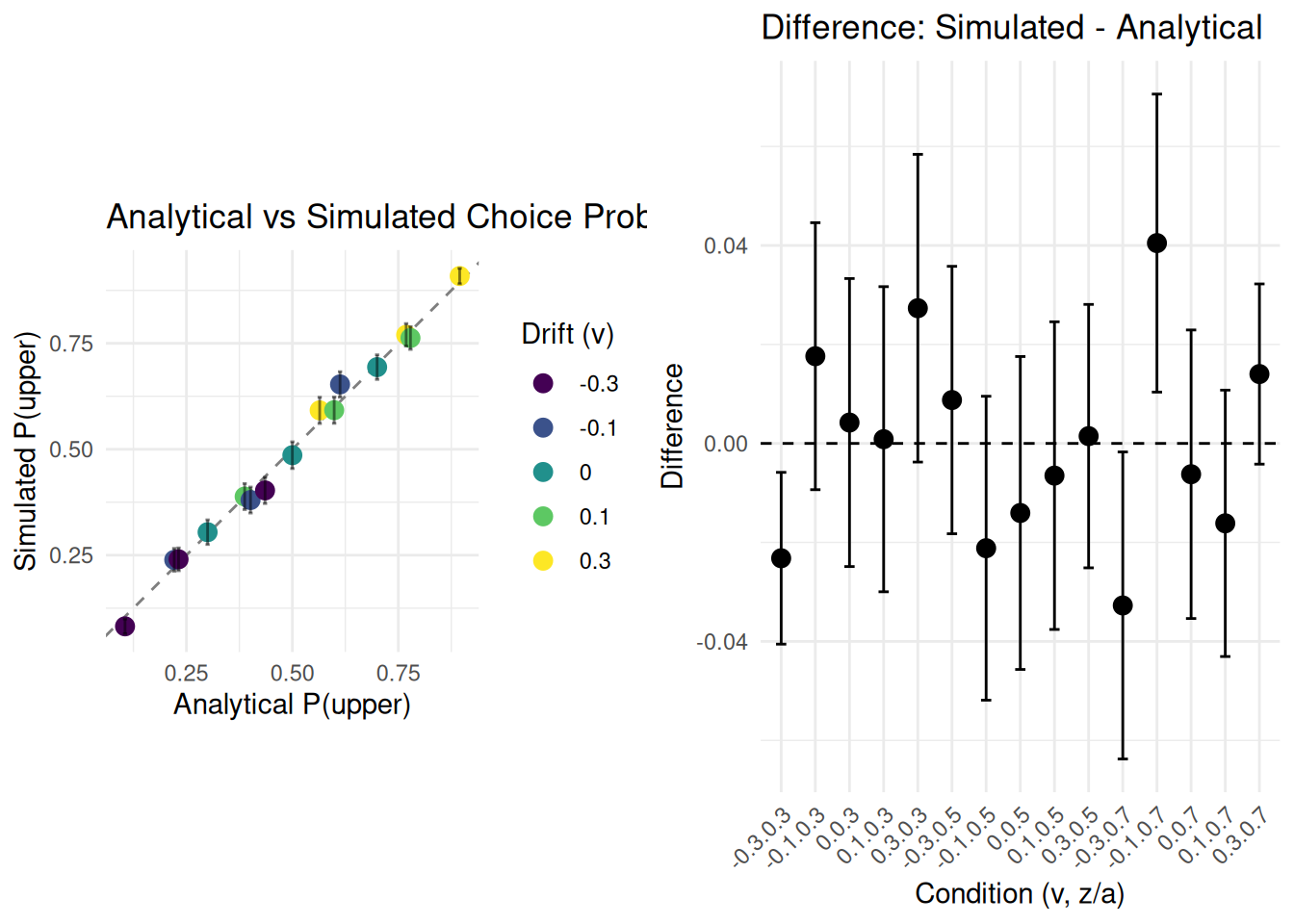

p1 <- ggplot(results, aes(x = p_analytical, y = p_simulated)) +

geom_abline(slope = 1, intercept = 0, linetype = "dashed", color = "gray50") +

geom_point(aes(color = factor(v)), size = 3) +

geom_errorbar(aes(ymin = p_simulated - 2*se_simulated,

ymax = p_simulated + 2*se_simulated),

width = 0.01, alpha = 0.5) +

scale_color_viridis_d(name = "Drift (v)") +

labs(title = "Analytical vs Simulated Choice Probabilities",

x = "Analytical P(upper)",

y = "Simulated P(upper)") +

coord_equal() +

theme_minimal()

p2 <- ggplot(results, aes(x = interaction(v, z_ratio), y = difference)) +

geom_hline(yintercept = 0, linetype = "dashed") +

geom_point(size = 3) +

geom_errorbar(aes(ymin = difference - 2*se_simulated,

ymax = difference + 2*se_simulated),

width = 0.3) +

labs(title = "Difference: Simulated - Analytical",

x = "Condition (v, z/a)",

y = "Difference") +

theme_minimal() +

theme(axis.text.x = element_text(angle = 45, hjust = 1))

gridExtra::grid.arrange(p1, p2, ncol = 2)

cat("Summary Statistics:\n")

cat(sprintf("Mean absolute difference: %.5f\n", mean(abs(results$difference))))

cat(sprintf("Max absolute difference: %.5f\n", max(abs(results$difference))))

cat(sprintf("All differences within 2 SE: %s\n",

all(abs(results$difference) < 2*results$se_simulated)))

}

verify_analytical_solution(n_sims = 1000)

## Summary Statistics:

## Mean absolute difference: 0.01565

## Max absolute difference: 0.04048

## All differences within 2 SE: FALSEObservation: The simulated proportion of choices for the

upper boundary should be very close to the analytically derived

probability. Any small difference is due to the stochastic nature of the

simulation and the finite number of trials. Increasing

n_sim_math_comp would typically reduce this difference.

This comparison provides a good validation for our basic DDM simulation

logic.

Analytical Solutions for RT Distributions

Analytical solutions also exist for the entire distribution of first passage times (RTs) for the simple DDM. These are often expressed as an infinite sum of terms involving exponential and trigonometric functions (e.g., see Ratcliff, 1978, Appendix; Feller, 1968; Cox & Miller, 1965).

For example, the probability density function \(g(t)\) for hitting the upper boundary \(a\) at time \(t\), starting at \(z\), given \(v, a, z, s\) (where \(s\) is the noise SD parameter as in \(dX_t = v dt + s dW_t\)) can be written as (e.g., Navarro & Fuss, 2009, adapting Feller):

\[ g(t|v,a,z,s) = \frac{\pi s^2}{a^2} e^{-\frac{vz}{s^2} - \frac{v^2 t}{2s^2}} \sum_{k=1}^{\infty} k \sin\left(\frac{k\pi z}{a}\right) e^{-\frac{k^2\pi^2s^2t}{2a^2}} \]

Implementing and accurately evaluating such infinite series can be numerically challenging (requiring careful truncation of the series and handling of potential underflow/overflow). This is one reason why direct simulation is often a practical and powerful approach, especially when across-trial parameter variabilities are introduced, as these often render analytical solutions intractable.

Why Simulation is Powerful

- Complexity: When across-trial variabilities

(

sv,sz,st0) are added to the DDM, or if more complex model features (e.g., collapsing boundaries, urgency signals, inter-trial dependencies) are included, deriving full analytical solutions for choice probabilities and RT distributions becomes extremely difficult or practically impossible. - Flexibility: Simulation allows us to explore these complex models by directly implementing the proposed generative process, step by step.

- Intuition: Simulating individual trials (as demonstrated with path visualizations in other vignettes) provides strong intuition about how the model behaves under different parameter configurations.

Our project leverages this power of simulation to understand the DDM, including its more complex variants with parameter variability, which are essential for modeling real-world behavioral data.

Conclusion

The Diffusion Decision Model is grounded in well-defined mathematics, typically expressed as a stochastic differential equation that describes the noisy accumulation of evidence. For simpler versions of the model (without across-trial parameter variability), analytical solutions for key predictions like choice probabilities and RT distributions can be derived.

Our simulation approach, based on the Euler-Maruyama method, provides a numerical approximation to this underlying continuous process. The close match we observed between our basic simulator’s output for choice probability and the established analytical prediction serves as a good validation of our core simulation logic.

For more complex and realistic DDM variants, especially those incorporating across-trial parameter variability, direct analytical solutions are often not available. This highlights the crucial and indispensable role of computational simulation methods in exploring, understanding, and applying these richer models to cognitive phenomena.